Bitcoin, the world’s largest cryptocurrency by market cap, tumbled below the $45,000 price level this morning, leading to a market-wide price carnage as a result.

Data further shows over $328 million worth of crypto positions were ‘liquidated’ this morning, with over 87,000 individual trading accounts affected. The market, however, seemed to temporarily stabilize at press time, putting a stop to what was the second sudden drop in as many weeks in the crypto market.

Come and gone

‘Liquidations,’ for the uninitiated, occur when leveraged positions are automatically closed out by exchanges/brokerages as a “safety mechanism.” Futures and margin traders—who borrow capital from exchanges (usually in multiples) to place bigger bets—put up a small collateral amount before placing a trade.

In traderspeak, ‘longs’ occur when investors are betting on prices of a certain asset to rise, while ‘shorts’ occur when they are betting against that asset.

Bitcoin ‘longs’ took a bulk of those liquidations this morning, data from analytics tool Bybt shows. $93 million worth of Bitcoin futures positions were liquidated, with $62 million—65% of all traders—of those being longs.

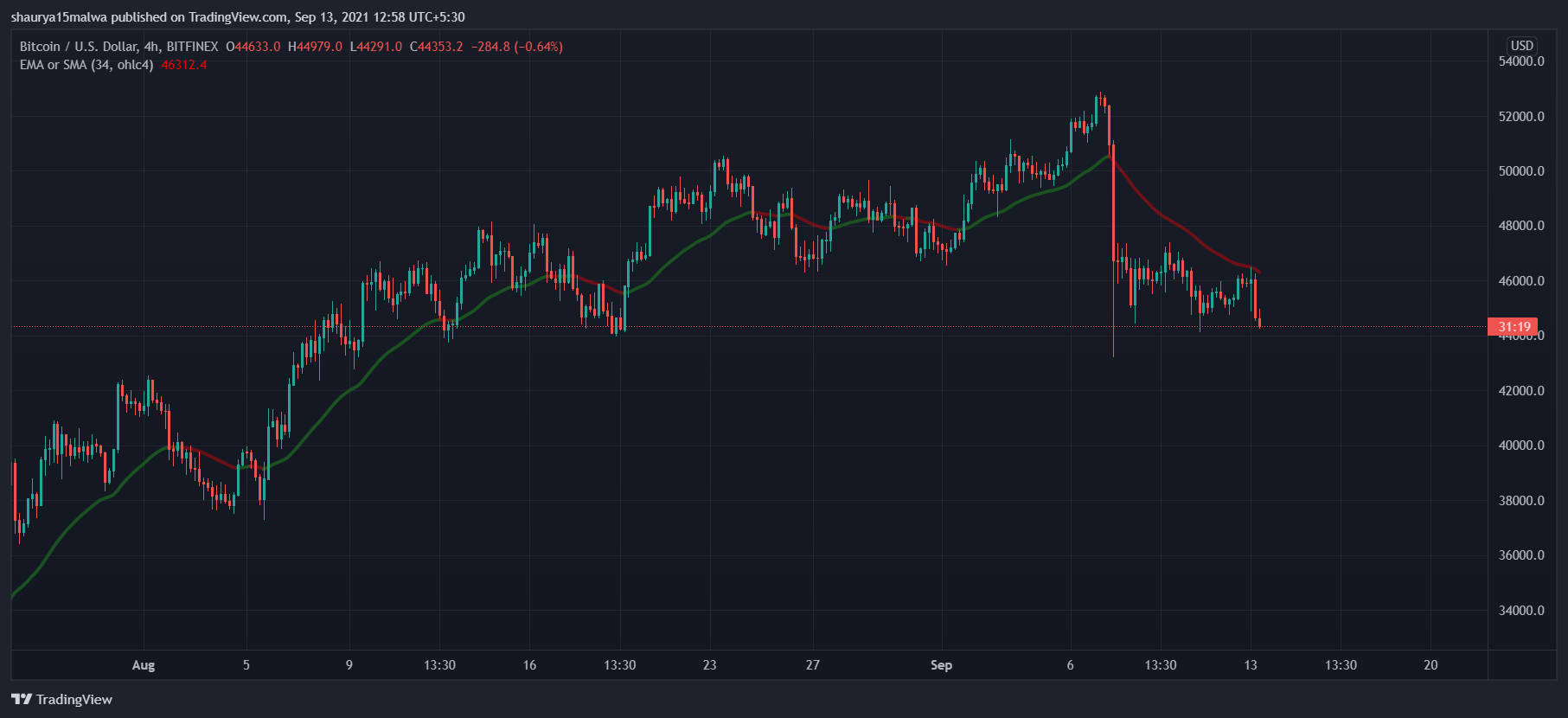

The overall trend seems to have slightly shifted as well. As the below image shows, Bitcoin broke below its $46,800 support to reach its current $44,200 support level. It has lost 13% of its value in the past week alone, and has the next ‘support’ level at $40,000 should prices fall further downward.

In terms of other cryptocurrencies, next in line with liquidations was Ethereum—with over $47 million worth of liquidations on ETH longs, accounting for $70 million in all. Solana, Cardano, Polkadot, and XRP followed ETH, with $26 million, $22 million, $12 million, and $10 million worth of liquidations respectively.

As such, Bybit took a bulk of all liquidations with $103 million, followed by Binance at $97 million, OKEx at $69 million, and FTX at $49 million.